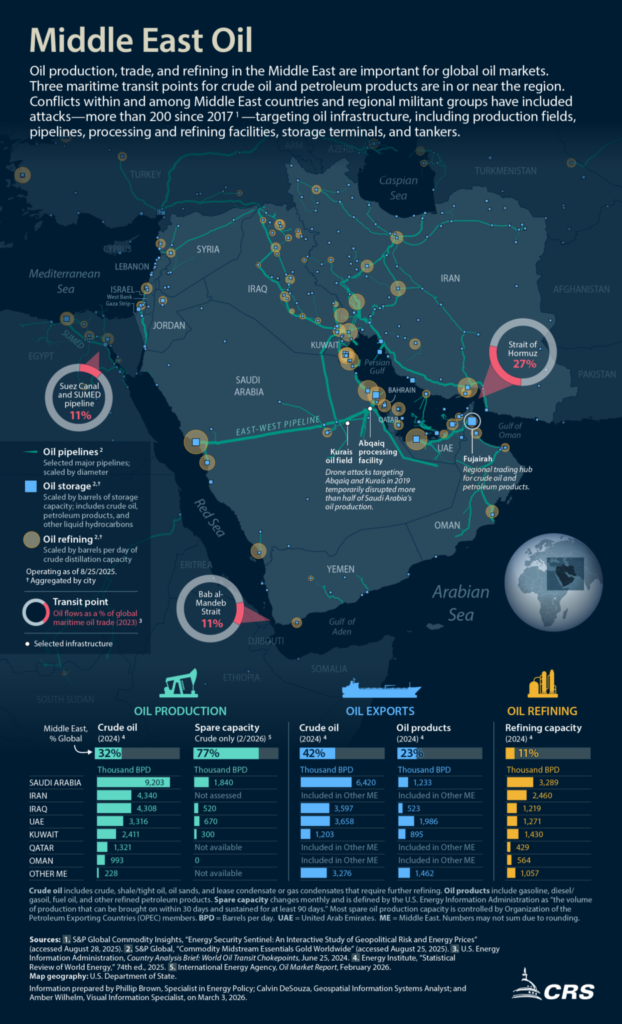

The illegal war launched by the United States and Israel against Iran has triggered the mother of all commodity-supply shocks. In response to the unprovoked onslaught, Iran’s closure of the Strait of Hormuz, the narrow waterway between Iran and Oman’s Musandam peninsula, has brought to a standstill the delivery of huge amounts of the world economy’s critical inputs.

Iran is the seventh country to undergo US military intervention in the first fifteen months of Trump’s presidency; five of these seven are rich in oil. Oil wars might make sense if American companies actually wanted to drill more. But they are hesitant to do so when oil is oversupplied and under-demanded. The raid on Caracas in January earned little interest among international oil majors, who were unenthused about the prospect of resuscitating Venezuela’s decrepit infrastructure and bitumen-like oil reserves, despite White House exhortations.

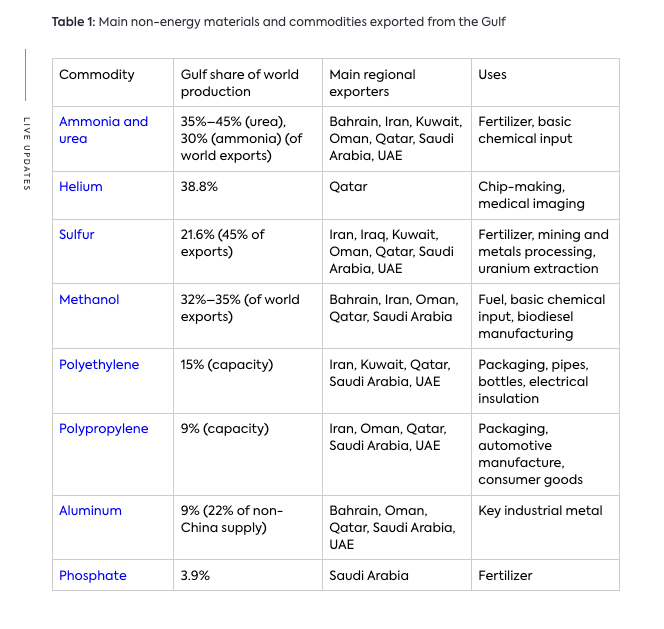

The world has never seen an interruption on this scale to the supply of stuff. It easily surpasses the 1979 oil crisis, sparked by the Iranian revolution, in which crude oil production declined by 4 percent. Forty-seven years later, Hormuz is the passageway for one fifth of the world’s crude oil and one fifth of its liquefied natural gas. It’s also the transit point for a third of exported urea—a feedstock used for making fertilizer which grows the food for an estimated half of the world’s population. Almost half of exported sulfur—used for fertilizer as well as extracting metals out of rock—are affected, as is helium, used for manufacturing microchips. Petrochemicals such as methanol and polyethylene are also being blocked.

The attacks on the Strait have not just stopped shipments. Thanks to strikes on oil and gas infrastructure, and a lack of storage, many companies have been forced to shut down production as well. It’s this that will ensure that shockwaves will continue to radiate long after the war ends. In many cases, restarting facilities won’t be fast, or predictable. Urea plants may take a couple of weeks to get back up; oil fields in Kuwait and Iraq may take as long as six months to start pumping again. Some of Qatar’s LNG capacity will be offline for years to come. Nothing can restart until Iran lifts its blockade. The long-term impacts remain to be seen, but they will no doubt be far-reaching and profound.

The war on Iran will be a reckoning of US military prowess. It may also undermine dollar centrality if Iran’s offer of safe passage for shipments invoiced in renminbi eventuates. In addition, this war will surely strike a blow to the prevalence of the global fossil energy system that the US dominates. Where once oil signaled stability and prosperity, this war will ensure that hydrocarbons will increasingly come to be seen as a vector of insecurity, intermittency, and scarcity, as the philosopher Pierre Charbonnier has argued.

A short war?

For now, global commodities markets are in Road Runner mode, and afraid to look down at the abyss. Prices of crude oil futures, LNG, fertilizers and other commodities have not even reached their nominal record levels. This comes in contrast to urgent warnings from experts in energy, fertilizers, shipping, and defense, all of whom warn that the scale of the coming crisis has yet to be registered. The IEA’s executive director has called the crisis “the greatest global energy security threat in history.”

If the market response has so far been fairly muted, that is thanks to persistent expectations of a short war. Oil markets were calmed by announcements about the US tying naval escorts to government insurance for ships, strategic reserve release, plus erratic declarations from Trump’s social media accounts about the imminent end to the war. The reaction illustrates a market consensus that over-indexes on the power of finance and US military power, and under-indexes on Iran’s resolve and asymmetric chokepoint power, and the physical vulnerability of production and logistics.

Oil markets are finely balanced, and there is little short-term “elasticity” on the consumption side. Certain levers are available to governments seeking to manage the supply shock, but with 20 percent of supply disappearing for an uncertain duration, and limited alternatives available, the world is now facing the possibility of “demand destruction” both in the short and long term. When demand is destroyed, consumption is suppressed—and often does not come back. Oil producers fear this phenomenon. It was a feature of the early 1980s, when oil consumption fell by more than 10 percent amid a recession that was partly caused by the 1979 oil crisis. In the aftermath of the 1979 crisis—which itself followed the oil price shock of 1973–74—countries like Japan and France built out nuclear power in order to cut their oil dependence, energy saving measures were mandated around the world, and cars became twice as efficient in the following decade.

Demand

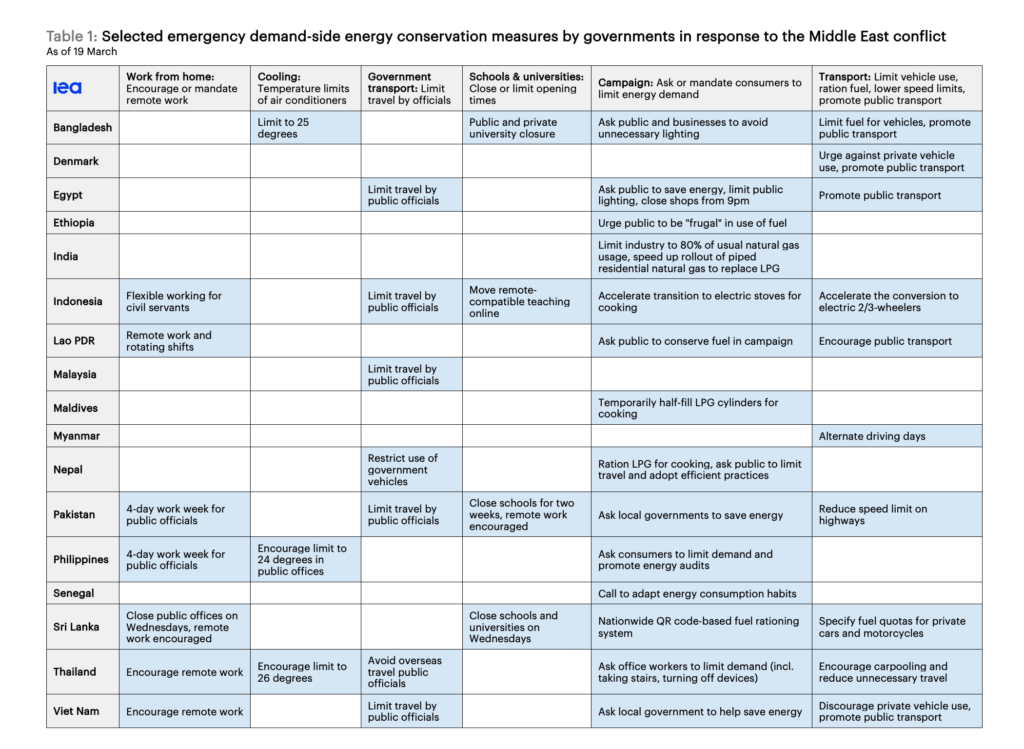

In Asian countries, which are the largest direct importers of Gulf hydrocarbons and refinery products, governments have already responded with Covid-style demand-side measures. Vietnam’s government has instructed people to work from home. Bangladesh has begun implementing fuel rationing and India has banned restaurants from buying liquified petroleum gas in an effort to prioritize supplies for households. The Philippines, which on March 20 said it had only forty-five days remaining of fuel supply, has declared a state of national emergency, which allows the government to make decisions about fuel allocation while strengthening enforcement against fuel hoarding and profiteering and compensating affected farmers.

These are temporary measures, but there are already signs of enduring policy shifts. The Philippines’ state of emergency includes longer-term intentions to accelerate the move to renewable energy, electric vehicles, and active transport. South Korea, too, has loosened its restrictions on renewables.

Asian and European countries are now competing over scarce LNG cargoes. In 2022 Europeans outbid Bangladesh and Pakistan over energy supplies, leaving them in the dark. In a stark reversal of these dynamics, at least eleven LNG ships en route to Europe were diverted to Asia this month, according to Kpler. In Bangladesh, four fertilizer plants have been closed and Petrobangla is buying spot LNG cargoes for between $23 and $28 per million BTUs—almost triple the price in December.

China, which usually supplies a third of Australia’s jet fuel and half for the Philippines and Bangladesh, has now banned fuel exports, prioritizing its home market. Australia is in line to receive special shipments of refined products from the US, but for some countries such preferential treatment (which comes at a steep price) is off the table. Thanks to its extraordinarily scant reserves, Australia will likely still have to restrict diesel sales, and some farmers are already postponing their crop seeding while they wait for deliveries of the fuel.

Energy security

Amid this supply shock, big changes in the energy complex now seem inevitable. Reduced demand will be one consequence and, with it, the accelerated shift away from dependence on an imported feedstock. The US will nonetheless continue to project its agenda of fossil-fuel dominance at home and abroad, but for countries that rely heavily on imported oil and gas—which is most of them—this conflict will raise an existential question: stick with hydrocarbon disruptions or build electric shock absorbers.

American hegemony relies on its military strength, its control of the reserve currency, and—more subtly—the regime of fossil fuels that it continues to impose on the world. This means underwriting the stability of oil flows, as well as limiting certain countries’ access to fuel markets as a disciplinary measure. The American promise of market reliability is provided by the US’s own production—its shale oil and LNG boom since 2010, and its commitment to sending “freedom molecules” to energy-starved Europe and Asia.

Energy experts agree that energy security—getting out of the grip of the US-led fossil order—will become the priority for many. The IEA has pointed towards a greater appetite for renewable energy sources—as well as for nuclear restarts and, in the short term, coal as emergency backup in Asia. Electrification will be crucial. Electric vehicles, heat pumps, and induction cooking all remove the need for constant imports (or constant purchases from domestic suppliers who can charge global prices). The UK government announced it would make solar panels and electric heat pumps mandatory in new building developments, and that it would speed up approval for “plug-in” solar panels.

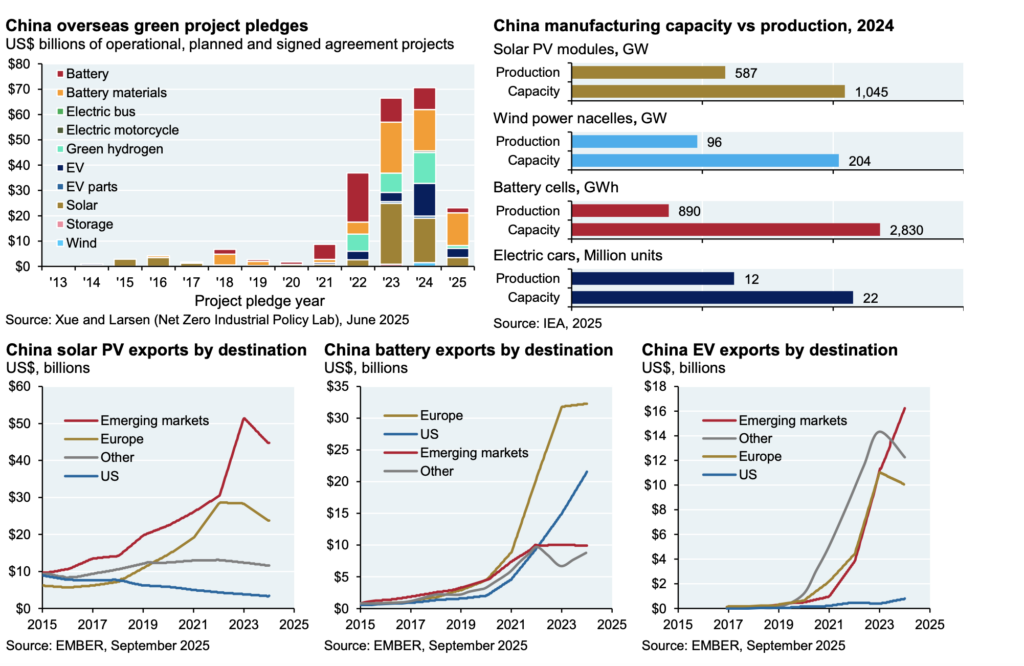

The American petrostate, which uses its power and influence in fossil fuels to discipline other countries, has a major competitor in China’s powerful electrostate. For now, China is working to cut its own dependency on fuel imports. Its surge of investment into the “new three”—EVs, batteries, and solar—was expected to crush oil demand by five million barrels a day by 2030. It is in the process of remaking the world’s energy order. It already makes four-fifths of the world’s solar panels—with a virtual lock on key inputs like polysilicon—which are being installed around the globe at a staggering rate. China’s largest EV brands are now household names in many parts of the world. BYD dealerships have been reporting a two-fold increase in EV orders since this war began.

Increasingly the US is not so much the gatekeeper of the world’s only energy system, but the paranoid guardian of an ailing oil order that is rapidly losing primacy. Clean energy alternatives are becoming more attractive, cheaper, and—most importantly—more reliable. China’s prolific production of solar panels, batteries, and electric vehicles is an increasingly viable alternative for many countries seeking to insulate themselves from ongoing disruptions in oil. Pakistan, for example, has already saved itself $12 billion thanks to the world’s fastest solar boom. How many other countries will follow suit? The bombardment of Iran, and the disruption it has caused to the fossil-fuel system, has drastically undermined America’s own agenda, but it may well pave the road to a greener, cleaner, and more secure energy future.